Strategy #2: This Simple 2-ETF Strategy Has Outperformed the Nasdaq for 13 Years

Full backtest, charts & strategy inside

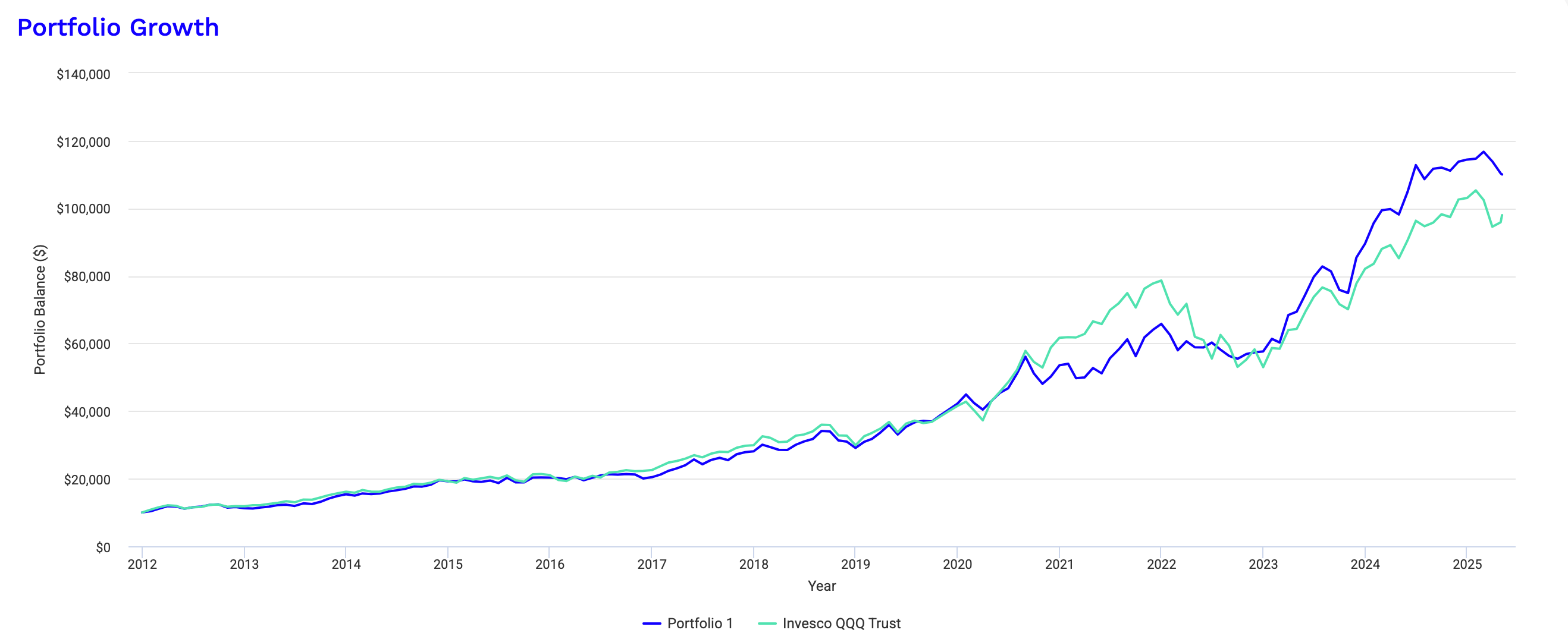

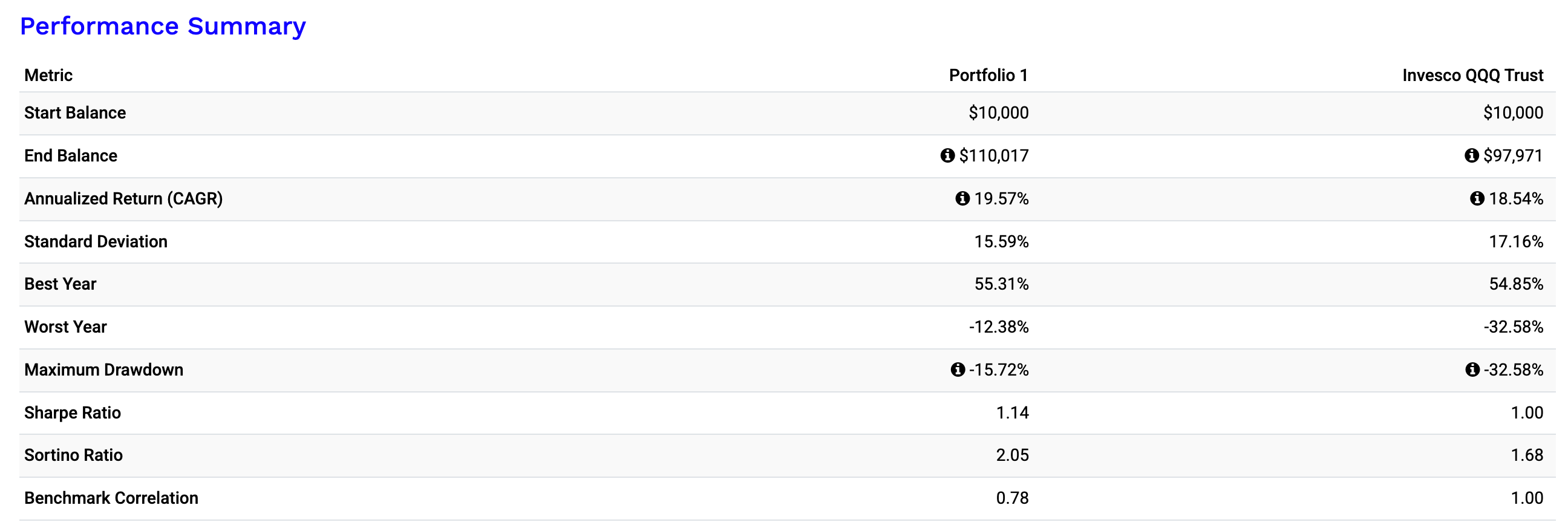

A once‑a‑year rebalance between an anti‑beta ETF and a 3× Nasdaq fund has compounded at 19.6 % since 2012 with a –15.7 % max drawdown.

The Tweet That Sparked It

A single chart from @thechartist on X showed a bored‑looking two‑ETF combo outperforming the Nasdaq for more than a decade. My first thought: no way something this simple prints almost 20 % a year. So I bookmarked it, ran the numbers myself and the results shocked me.

Key result: Strategy (Portfolio 1) vs Benchmark (Nasdaq)

19.6 % CAGR, -15.7 % max drawdown, Sharpe 1.14 (2012‑2025)

Why “Set‑and‑Forget” Still Fails Most Investors

Even with hundreds of low‑fee ETFs on the market the typical buy‑and‑hold portfolio crawls in at 8–10 % CAGR and endures pretty deep drawdowns, probably deeper than most people expect and can handle.

Deep crashes: QQQ sank –35 % in 2022 before clawing back.

Emotional panic: 10–20 % drops in days trigger bottom‑selling.

The Strategy: One Annual Rebalance

Allocation

67 % BTAL – market‑neutral, short‑beta exposure

33 % TQQQ – 3× leveraged Nasdaq exposure

Once a year, first trading day of January I restore those weights. Five minutes, done.

I really like simplicity in strategies, but is this too simple?

Backtest (2012‑2025)

• 19.57 % CAGR

• –15.72 % max DD

• Sharpe 1.14

8 of 13 years beat the Nasdaq.

Since I typically doesn't trade rotational strategies or ETFs I am not using my standard platform ProRealTime for this backtest, I am using Portfoliovisualizer.com.

Why It Works

Anti‑beta hedge – BTAL spikes when high‑beta names crash.

Leverage efficiency – 33 % TQQQ equates to ~99 % Nasdaq exposure while BTAL hedges downside.

Execution simplicity – It’s simple, therefore easy to follow.

Comparing Rotation Frequency: Annual vs. Quarterly vs. Monthly

Annual rotations set the baseline but what if you rebalanced more often? Here’s how frequency shapes returns and risk.

Annual Rotation Baseline (Calendar Year)

• Results (2012–2025): 19.57% CAGR, –15.72% max DD, Sharpe 1.14

Quarterly Rotation Test

• Results (2012–2025): 17.28% CAGR, –23.45% max DD, Sharpe 1.06

Monthly Rotation Test

• Results (2012–2025): 16.24% CAGR, –25.09% max DD, Sharpe 1.03

At first glance you’d expect quicker rotations to fine‑tune exposure and squeeze out extra return. But as you can see, the backtest shows the opposite.

So, what’s going on?

Anti-Beta Timing Advantage

BTAL spikes when high‑beta melts down, but those spikes are lumpy and rarely last just 30–90 days. An annual reset lets the anti‑beta hedge fully do its job before you clip gains.

Volatility drag on TQQQ

Leveraged ETFs pay you when the index trends, but path‑dependence penalises whipsaws. Higher‑frequency rebalancing forces you to rebuy TQQQ after every mini‑pullback, compounding decay.

Bottom line: in this specific pairing, patience beats tinkering. One calendar‑day on your January checklist handily outperforms 4- or 12‑times‑a‑year micromanagement, delivering higher returns, smaller drawdowns, and more free weekends.

Footnotes & Disclaimers

Backtests run on PortfolioVisualizer, January 2012 - May 2025, total return series.

Educational content only. Nothing here is financial advice.

apologies for being a bit outspoken. You can backtest what you want, but if you don’t take into account market regimes you get misled and you mislead (yes, inadvertently). All of your backtest time is one where disinflation prevailed with one exception (2022), and guess what? By picking assets that perform well under disinflationary conditions, and leveraging one of them a lot, you do well. You can’t generalise like that, that’s why backtests cannot be used to prove that something works, but only that in that sample path nothing ugly came up (yes, that’s all you can say). In 2022 the strategy suffered as inflation spiked. While in all other periods Treasuries were an exceptional asset class as the Fed splurged on monetary easing with repeated QEs, till there was QE4 with Covid. For the same reason the Nasdaq, the asset you want to leverage so much, outperformed being a long-duration asset. Can’t you see how unique those conditions were? Your backtest tells you only this: if long-duration assets will do well, i can do well with this simple model. And it is not even a rotation strategy, as you are always invested in long-duration assets. Rotating from red into pink is not much of a rotation. Wait and see when inflation comes back. You’ll tell me what happens. Can’t you see that dollar-centric assets have started to underperform for secular reasons, and that your strategy is basically an overweight on US assets that perform well when the dollar rises? Plot Nasdaq/MSCI World xUS against real trade-weighted US dollar. When the world flocks to Nasdaq and Treasuries it has to buy dollars to do that. Hence, dollar (real trade-weighted) and Nasdaq relative to other global markets tend to move together. Your bet is a huge one on disinflation and perpetual US exceptionalism. US exceptionalism is done with, as fiscal and monetary capacity are gone (too much debt and future stagflation with tariffs), and the stimulus impulse is shifting to Europe and China. Trump has upended US exceptionalism with tariffs, and does not want a strong dollar. Markets in the future will not be as US -centric, and your backtest takes you straight into that and you’ll be headed for heavy losses once the regime changes. Under the new regime you’ll have to consider inflation hedges (gold, commodities) and shorter-duration assets. At least you will have to be careful to use Nasdaq leverage only when disinflation is there. How do you measure it in real time? With an oil-to-gold ratio. Yes, now we have a short spell of disinflation according to that ratio … You get the gist. This comment is already way too long

This is a great representation of the strength of BTAL. The problem is the short history. This 17 year period is an exceptionally strong market. We don't really know what it will do in an extended down market, as occurred in the 30's-40s, the 70's or even 2000-2008.

Your comments on why annual rebalancing works for this are spot on!