The Backtesting Blueprint - How to Avoid Costly Mistakes and Build Profitable Trading Systems

Don't let your "perfect" backtest mislead you.

Did you know that nearly 80% of new algorithmic traders fail within the first year? It's a harsh reality. You pour your heart, time, and money into crafting a seemingly perfect trading system. You dream of automated profits rolling in while you sleep.

Then, reality hits like a ton of bricks.

The system that looked so promising in backtesting… tanked in live trading.

The truth is this:

Backtesting is absolutely crucial.

But it's also incredibly easy to mess up. A tiny mistake in your backtesting methodology can lead to false confidence. And that false confidence can cost you dearly.

This post will discuss some common backtesting pitfalls. l will show you how to avoid them. And you will be able to build trading systems that not only look good on paper but also perform in the real world.

Think of this as your survival guide to the backtesting jungle.

You'll understand how to read results with a critical eye and you'll increase your odds of creating a robust and profitable algorithmic trading system.

Why Your "Profitable" System Might Still Fail

Backtesting is like looking into a crystal ball.

But crystal balls can be cloudy, distorted, and downright misleading if you don't know how to use them.

The problem?

Many traders blindly trust backtesting results. They see a nice, smooth equity curve and assume they've found the holy grail.

I've seen it happen time and time again. A trader spend weeks, even months, optimizing a system to perfection on historical data. Every parameter is tweaked, the backtest looks incredible. High win rate, low drawdown…

Then comes live trading….

Disaster.

The system unravels. Profits evaporate. And the trader is left scratching their head, wondering what went wrong.

The issue is not that backtesting is useless. It's that traditional backtesting is often flawed. It creates a mirage of profitability.

But what if I told you there's a better way?

A way to backtest with robustness in mind, with skepticism, and with a deep understanding of the limitations. A way to build systems that are not just optimized for the past, but robust enough to handle the future.

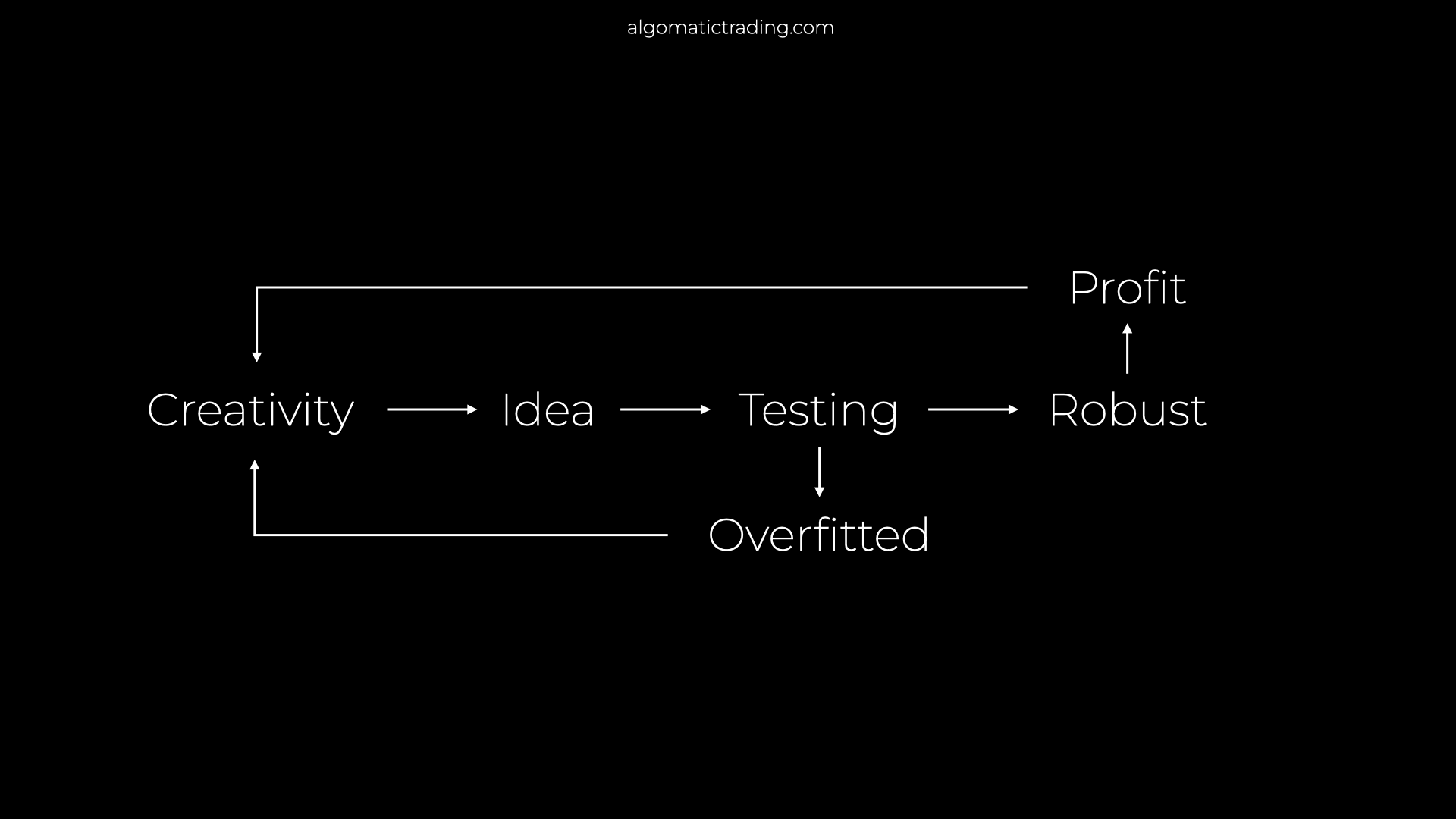

I call it Robust Backtesting.

Robust Backtesting is not about finding the perfect system. It's about understanding a system's strengths, weaknesses, and its breaking points. It's about stress-testing your ideas.

It's about preparing for the unexpected.

When I started using Robust Backtesting, everything changed. My systems became more reliable. My confidence grew. And my trading results improved dramatically.

Here's the "aha!" moment:

Backtesting is not about finding a guaranteed path to riches. It's about risk management and informed decision-making.

If you treat backtesting as a box-ticking exercise, you're setting yourself up for failure. But if you embrace Robust Backtesting, you'll gain a massive edge in the market.

The Robust Backtesting Blueprint: 5 Steps

"Without data, you're just another person with an opinion." - W. Edwards Deming

That quote underscores the critical role of data and testing in trading. Robust Backtesting isn't a one-time event. It's a process of continuous improvement. It's about constantly challenging your assumptions and refining your process based on new data and insights.

Here’s your blueprint to bulletproof your system:

Actionable Step 1: Choose Representative Data

Many traders use limited or biased historical data for backtesting. Maybe they only test on a few years of data, or they only test during a bull market.

Your backtesting data should be representative of the market conditions you expect to encounter in live trading. Test on different time periods, including bull markets, bear markets, and periods of high volatility.

Here's what I want you to do:

Get access to high-quality historical data that spans a long period and includes different market regimes. If you're trading stocks, test on a broad market index like the S&P 500 but also similar markets like Nasdaq.

Actionable Step 2: Account for Slippage and Commissions

Get a more accurate picture of potential profitability.

Neglecting transaction costs can lead to unrealistic backtesting results. Slippage (the difference between the expected price and the actual price) and commissions like overnight fees for CFD trading can eat into your profits.

Here's what I want you to do:

Incorporate realistic slippage and commission estimates into your backtesting model.

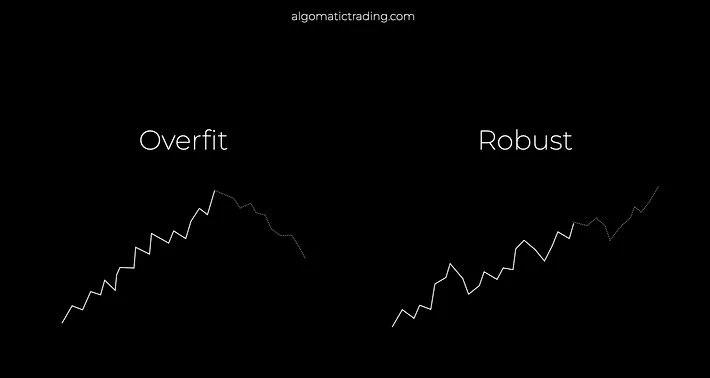

Actionable Step 3: Avoid Overfitting

Build a system that's more likely to work in the future.

Overfitting occurs when you optimize a system too much to historical data, making it fragile in live trading. The system becomes too specialized to the past and fails to generalize to new data.

Here's what I want you to do:

Use techniques like simplicity, cross-validation, and walk-forward analysis to prevent overfitting.

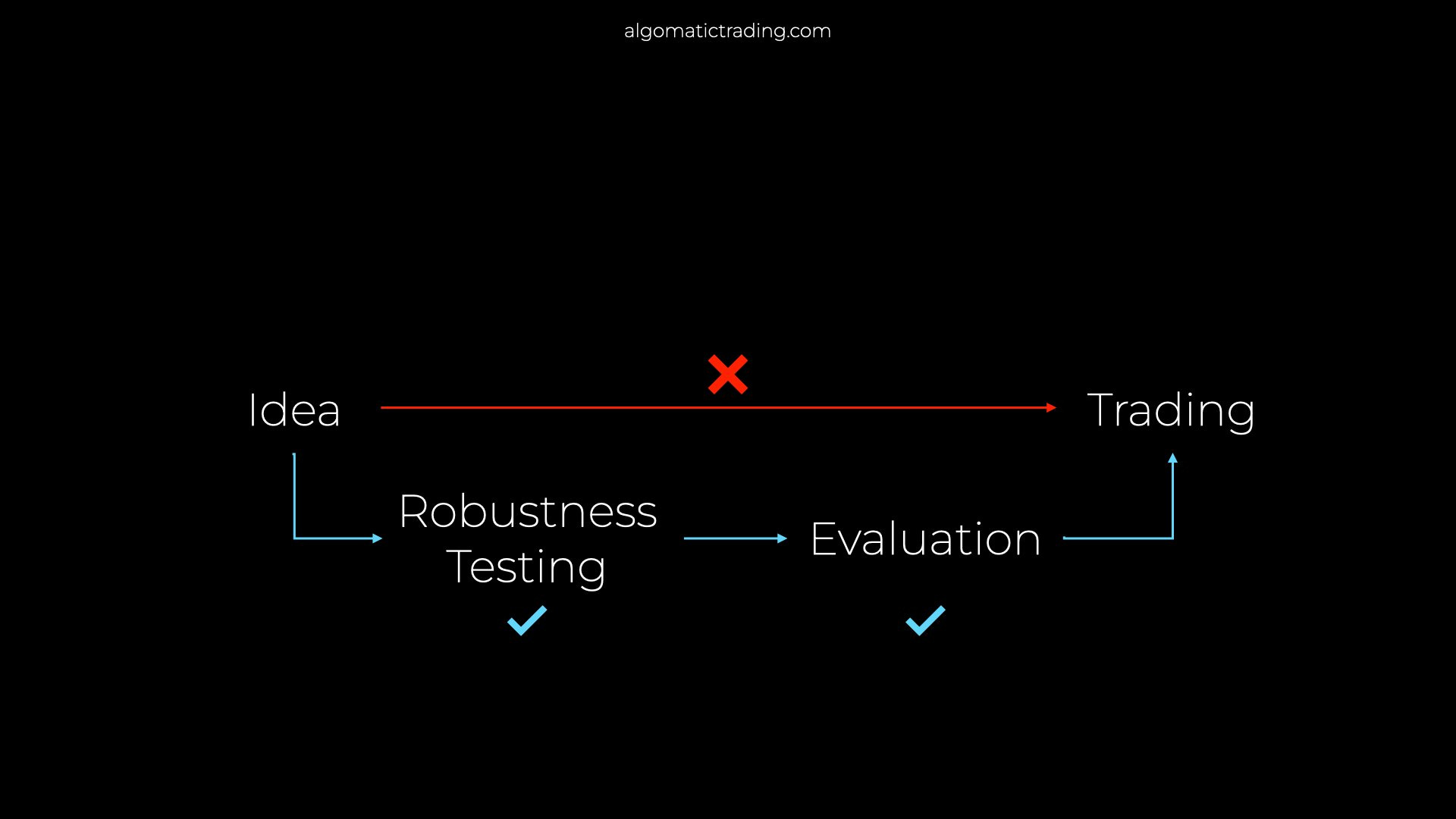

Actionable Step 4: Walk-Forward Analysis or Out-Of-Sample

Get an objective view on how the system will perform over time.

Traditional backtesting optimizes on all available data, which can lead to overfitting.

Walk-forward analysis simulates forward testing by optimizing on past data and testing on unseen data.

Here's what I want you to do:

Divide your data into training and testing periods. You can easily do this manually by dividing 50-70% of your existing data to a section that you will test your system on and then save the remaining data for a single final test to evaluate the strategy, after this last Out-Of-Sample test you can't change any parameters or you risk overfitting. Optimize your system on the training period and then test it on the testing period.

Actionable Step 5: Stress Test Your System

Identify weaknesses and make the system more resilient.

Most backtests are conducted under "normal" market conditions. But what happens when the unexpected occurs? A flash crash, a black swan event, or a sudden spike in volatility?

The solution is to stress test your system under extreme market conditions to see how it holds up.

Here's what I want you to do:

Subject your system to a range of stress tests, including:

Sudden price shocks

High volatility

Gaps in the market

Unexpected news events

Some great time periods for this could be 2000-2001, 2008, 2020, and 2022.

If you want to start trading with algos, our recommended platform is ProRealTime. You can backtest all the way back to the 1980s and get all necessary statistics from their valuable backtest reports.

Disclaimer: I am not a financial advisor. This article is for informational and educational purposes only. Trading involves risk, and you can lose money. Always do your own research.